Reaching the forefront of Gen AI in banking – by decoding “Voice of customer” on Social media interactions

When Gen AI emerged as the next leap in technology in early 2023, organizations faced pressing questions on its most effective applications. Many of them have grappled with how to integrate and scale the technology, and the potential business value impact of its use cases.

Within banking industry, while initial Gen AI pilots and efforts focused on productivity, recent challenges and use cases are more focused on answering how this technology could alter customers interactions with the banks, and the execution of various job functions.

A recent study by McKinsey Global Institute highlights that the banking sector stands to gain significantly from the adoption and use of Generative AI, with potential value creation estimated at $200-340 billion annually. From this, ~20-30% of the gains are projected to come from retail and corporate banking each.

The potential value creation from the adoption of Generative AI is estimated to be $200-$340 billion annually

Strategically implementing customized Gen AI solutions allows financial institutions to significantly elevate the overall customer experience and improve service operations.

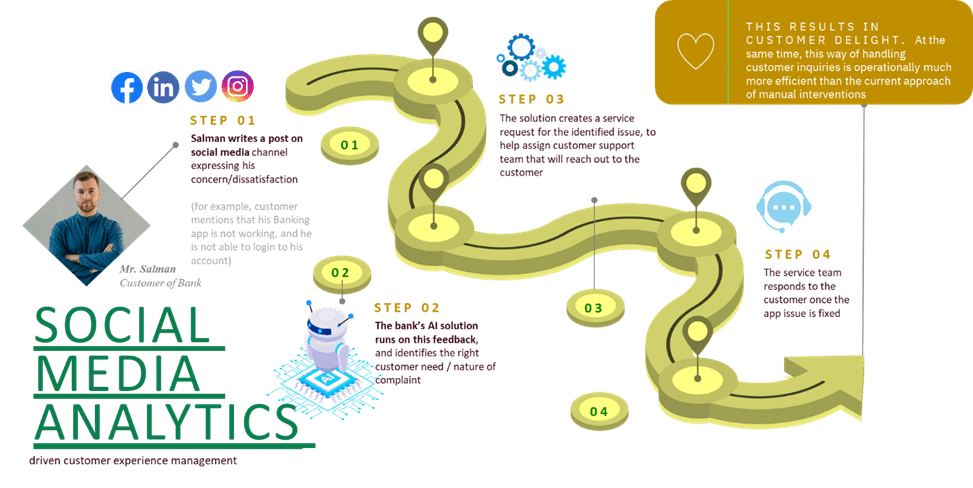

One key area on which our team has been collaborating with various banking clients, is to leverage Gen AI to provide better customer assistance, especially on social media touchpoints.

While 40-45% banking customers have traditionally voiced their issues using channels like chatbots on mobile app/online banking, or by speaking to a live agent (~20%), they are increasingly turning to social media platforms, online reviews, and customer service mails, to raise their voice more openly and intensely.

Customers are increasingly turning to social media platforms, online reviews

Coupled with this is the fact that banks have generally been behind the curve in terms of developing effective technology solutions or bespoke tools, to manage social media interactions: Some of the key challenges that have persisted in this area include:

-

-

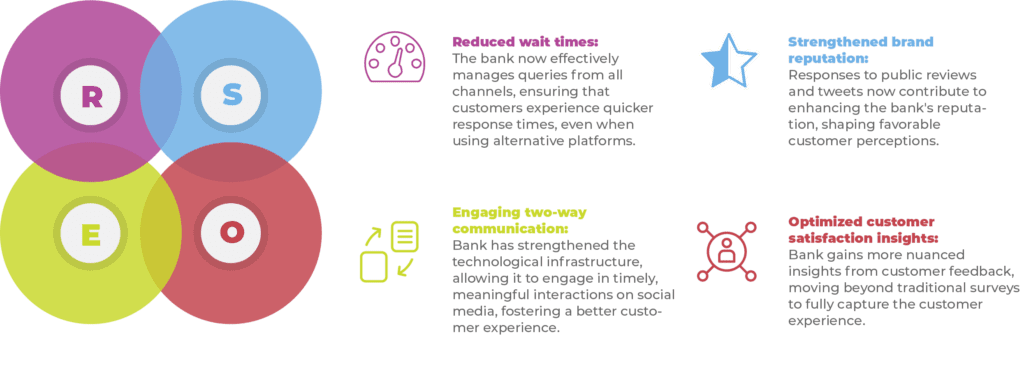

- Longer wait times: The bank may prioritize complaints or queries raised through traditional channels first, potentially leading to extended wait times for customers using alternative platforms

- One way communication: Social media interactions have often been a one-way street, with many banks lacking a strong technological foundation to prioritize and respond to these interactions promptly

- Brand reputation risks: Public tweets and reviews on platforms such as Google can have a significantly negative impact on brand perception, influencing the opinions of other customers

- Missed opportunities in satisfaction assessment: while banks have continued to rely on customer surveys for NPS and CSAT, there is untapped potential in leveraging Gen AI applications, to truly understand the “voice of customer” from their feedback

-

Given this context, our engagement aimed at helping the bank design and implement a gen AI solution, which could identify the key pain areas using customer interactions and feedback on social media, and recommend the right action automatically to solve the issue.

However, implementing generative AI comes with certain risks. It cannot be deployed as an out-of-the-box solution; it requires careful customization to ensure the responses are contextually relevant. Additionally, clear guardrails must be established to mitigate communication risks and ensure that the AI operates within defined boundaries.

Implementing generative AI comes with certain risks. It cannot be deployed as an out-of-the-box solution.

We have addressed these challenges by carefully embedding personalization into our Gen AI solution. The model and aspect identification have been tailored to align with the bank’s specific data and downstream communication plan.

Technical solution approach

Further below are details of our technical solution approach and the model architecture:

-

-

- Data collection – historical data for all customer complaints, sales inquiries and queries, from various social media platforms such as X, Facebook, LinkedIn, Instagram etc.

- Data pre-processing –

- Data cleansing and tokenization (using a pretrained transformer tokenizer)

- Text encoding and batch creation with random sampling

- Applying language detection models (such as NLLB200 from Meta) for translating non-English languages such as Arabic into English

- Intent recognition – training and customizing a LLM to identify sales leads and complaints from the customer interaction texts. The details of the modeling approach is present in the subsequent section

- Categorization and aspect extraction – extract the specific product and service-related context for which the customer is reaching out

- Output generation for downstream integration – exposing the model output to seamlessly integrate with the bank’s systems, either by creating service request tickets within the complaint management system or by generating sales leads for CRM integration

-

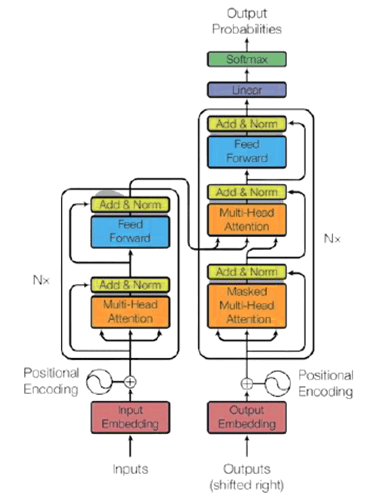

Model architecture:

Our team trained and customized a BERT (Bidirectional Encoder Representations from Transformers) model, to identify intent of customer interaction text.

- Bidirectional: Considers context from both left and right sides of the target word

- Pre-trained: Trained on a large corpus to capture diverse language patterns

- Transformers: Utilizes transformer architecture for efficient processing

Some of the key model components were:

- Encoder: Multi-layer transformer blocks that process input text

- Input Representations: Combines token, segment, and position embeddings

- Output Representations: High-level representations for downstream tasks

The model was trained using a relatively small sample of ~10,000 historical data points (since a pre-trained model doesn’t require a large no. of data points), by using 12GB CUDA enabled GPU system.

Model training approach:

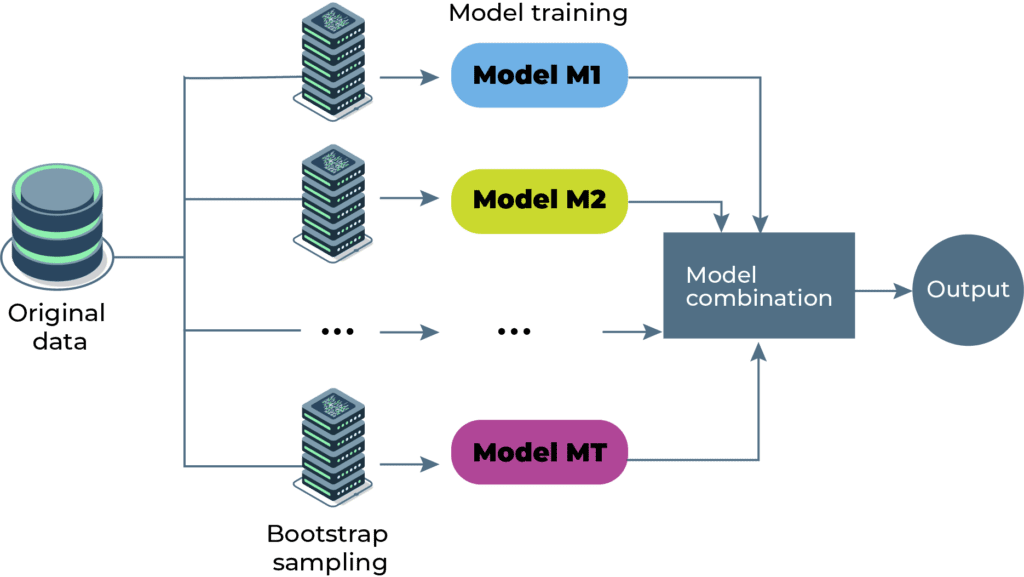

Model bootstrapping and hyperparameter tuning:

For bootstrapping, team used the following steps:

- Model inference – applying model on unlabeled dataset and getting prediction probabilities

- Filtering uncertain predictions and expanding dataset by adding new predictions

- Model fine-tuning based on new dataset

- Evaluating performance on validation and test data-sets, including cross-validation

Hyper-parameter tuning:

We performed hyperparameter tuning using the following approach:

-

-

- Iterations based on Optimizers (AdamW, AdaFactor), Batch size (4,8,16), # of epochs (10, 20, 30, 40, 50), and learning rate (10-3, 10-5)

- Grid search for the iterations

- Evaluate performance across precision, accuracy, F1 score, recall etc.

- Choose the best performing hyper-parameters

- Fine-tune the BERT model on full training dataset

-

For topic extraction, our team worked with two approaches :

TF-IDF analysis:

Latent Dirichlet allocation (LDA):

Impact and outcome:

Our team was able to create significant value for our banking clients in 3 key areas:

-

-

- Improved sales potential: Within first few months of implementation, the solution identified several hundred incremental sales leads for cards and loans each month, from prospects expressing interest on social media

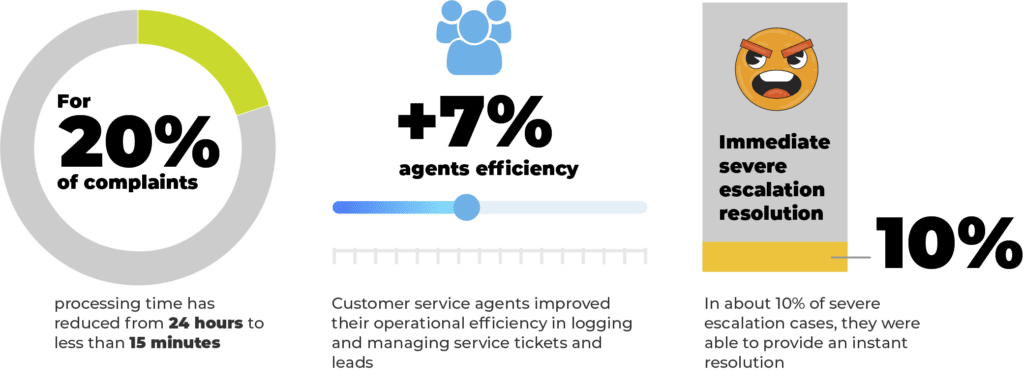

- Enhanced customer experience: The bank’s customer service team reduced the average response time for nearly 20% of complaints from 24 hours to less than 15 minutes. In about 10% of severe escalation cases, they were able to provide an instant resolution

- Agent performance: With clearer insights into customer intent and context, customer service agents improved their operational efficiency in logging and managing service tickets and leads by 7-8%

-

As the solution continues to evolve, we are collaborating with our banking clients in using gen AI for further enhancing customer experience by:

-

-

- Generating insights from customer feedback and ratings given on Google for specific branches, products and services

- Instant trend detection for monitoring shifts in customer opinion and engagement patterns in real time, allowing the bank to quickly adjust its communication strategy

- Automated summarization: Assisting bank’s call center agents by automatically summarizing notes taken during customer interactions, streamlining the process of servicing calls

- Tracking interactions: identifying influential users or brand advocates, allowing the bank to engage effectively with key stakeholders and manage its online presence

-

About the authors:

- Saurabh Assat, Partner, Sutra Dubai

- Ravi Saroj, Technical Expert, Sutra Delhi, India

- Rahul Bijarniya, Senior Consultant, Sutra Delhi, India